Earshare: The Idiot's Guide to Investing in Spotify

Earshare: The Idiot's Guide to Investing in Spotify

Per My Last E-mail #41

If you’re reading this but you aren’t subscribed to Not Boring, it’s time to join 1,825 people who have a blast while learning about business strategy, trends, and events.

Hi Friends 👋,

Happy Monday! I spent the weekend knocked out by a cold, which it turns out is the only thing with the power to make Per My Last E-mail shorter!

I only had the energy for two sections this week:

Earshare: Per my last e-mail, I started writing my bull case for Spotify, and ended up writing about why 99% of us should probably ignore numbers and invest based on narrative.

Links & Listens: Investing in experiences, two ways; deceptively simple business equations; why we use corporate jargon.

That’s all I got. Let’s get to it.

Earshare: The Idiot’s Guide to Investing in Spotify

(Rule #1: When you’re writing about Spotify, you need to embed Spotify.)

You Shouldn’t Stockpick, but if You’re Going to Anyway…

Trying to beat the market by picking stocks is idiotic. Even sophisticated investors struggle to outperform, and most of us aren’t very sophisticated. In 1973, Princeton professor Burton Malkiel wrote in A Random Walk Down Wall Street, that “A blindfolded monkey throwing darts at a newspaper's financial pages could select a portfolio that would do just as well as one carefully selected by experts.” More recent studies have shown that Malkiel may have underestimated the monkeys.

Yet here we are. Most of us have at least a small percentage of our net worth in a portfolio of stocks that we pick ourselves, because even though investing in a mutual fund or an ETF that tracks the S&P 500 is the right move in the long-run, in the short-term, it’s kind of boring. We’re human, not calculators, and we want to show that we actually are a little bit smarter than those other guys who lose to dart-thowing monkeys.

So if we’re going to do it anyway, we might as well take advantage of our human ability to understand stories, and leave the fancy numbery stuff to the calculators. My thesis is that most of us shouldn’t even bother with the numbers, and should spend that brainpower on understanding the narrative.

The numbers are all priced in, the upside is in the narrative.

What I mean is that all of the sophisticated investors have access to the same data and run similar models on it. The current price of a stock is reflective of all of that information. It’s exceedingly rare for an individual to beat the pros and their computers by understanding a number better than them. Machines are really really good at numbers. They can find and incorporate a new data point before a human even knows to start looking.

But humans are the best at stories. I think that understanding the narrative around a stock, and taking a view on how other humans might react to information that confirms or challenges that narrative is the regular person’s best shot at picking winners.

It’s Peter Lynch’s “Invest in what you know” for the stories the market tells.

Which brings us to Spotify, a long-time favorite product and my new favorite investment.

What’s Wrong With Spotify?

Until this past week, the market has been on an incredible run. The S&P 500 is up 5.7%, and the NASDAQ is up an astonishing 12.8%. The internet behemoths that compete in content - Netflix, Amazon, Google, and Apple - are up 3.3%, 12.7%, 17.4%, and 56.2%, respectively. (These numbers were a lot more impressive a week ago…)

Meanwhile, the company whose product I spend more time in than all four of those combined is down over the past year. Spotify has lost 0.7% over the past 12 months, and 17% from its April 2, 2018 IPO day closing price.

The narrative around Spotify is that it is in a weak negotiating position with record labels which limits the amount of money they’re able to earn from each subscription.

In its current state, it is essentially a marketplace business with little leverage over the supply side, the labels who own the valuable back-catalogs of music that the demand-side of the marketplace demands. Spotify pays about 70% of subscription revenues out to the labels for the right to stream their artists’ music, which leaves it with very little to cover the costs of acquiring new users, building and maintaining products, putting its team up in fancy digs at 4 World Trade Center and do all of the things it takes to run a business. That means that Spotify has underperformed expectations since going public, and has lost money in every year since its founding (it had a $73 million operating loss in 2019).

Despite all of the love that consumers have for the brand, investors have viewed it as a low-growth, low-margin, money-losing business with declining revenue per user and aging brand loyalty. And by the way, they’re going head-to-head with companies who do nothing but spit off cash that could be used to crush them: Apple, Google, and Amazon.

Yikes, right? Well here’s the thing. Everyone has that information. The negative stuff is all priced in.

The Long Game and the Triple J-Curve

We can’t rest on our laurels. We believe the market we’re going after is audio. That adds up to 2-3 billion people around the world who want to consume some sort of audio content on a daily or weekly basis. If we’re going to win that market, we’d have to be at least a third of it. We have somewhere between 10-15x of where we are now of opportunity left. We’re still in the early days of our journey.

Spotify CEO Daniel Ek on Invest Like the Best

When you look at all of Spotify’s moves, you need to keep one main thing in mind:

Spotify is playing the long game.

The company believes that audio is going to be massive, and they are making moves to own audio. The trends support them.

AirPods are the single most popular product Apple has ever made and the most popular headphones in the world. Apple sold 15 million AirPods in 2017, 35 million in 2018, and 60 million in 2020.

Smart speaker sales nearly doubled between 2018 and 2019, from 86.2 million units to 146.9 million units.

Connected car units reached an estimated 51 million units in 2019, up 45% from 2018, and are expected to reach 76 million units by 2023.

To Spotify, playing the long-game means being the leader in audio by the time it really hits its stride, and having a business that is structurally set up to capture profits when that time comes.

To win the long-term, sometimes you need to do things that look really bad in the short-term.

You treat music as a loss leader: give in to record labels’ demands in order to acquire the songs that help acquire customers.

You swallow declining revenue per user: acquire customers on free plans to grow users.

You overspend for your next big thing: buy The Ringer for $250 million, after spending nearly $400 million to acquire Gimlet Media, Anchor, and Parcast.

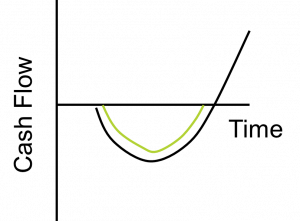

Spotify is putting itself through a triple J-curve.

A J-curve is so named because it looks like a capital J. It occurs when a company spends money upfront on something that will take a long time to pay off, but when it does pay off, it pays off really well.

You see the J-curve a lot in Software-as-a-Service (Saas) businesses. Here’s a very oversimplified example: your company hires a sales guy for $150k to acquire a customer who starts off paying $10k per month. For the first 15 months ($150k/$10k), your financials look bad. For a while, you’re spending money and not making any, and even when you start making money, it’s nowhere near what you invested. But over time, as the company remains a loyal customer, and starts spending $20k and then $30k and so on for months, your initial investment pays off multiple times over. Investors realized that this worked in a predictable and repeatable way, and SaaS companies have been some of the most successful IPOs of the last few years.

Spotify is doing something similar, but with consumers, who are less predictable, and without a clear precedent outside of Netflix, which is itself still pretty unclear.

Spotify’s triple J-curve is comprised of two customer acquisition J-curves and one backward integration J-curve.

They are agreeing to financially unfavorable deals with record labels to acquire customers, hurting margins in the short-term.

They are using 90 day free trials to acquire listeners, hurting revenue per user and while increasing payouts to labels in the short-term.

They are spending hundreds of millions of investors’ dollars to acquire podcast companies with no clear way of monetizing in the short-term.

The customer acquisition J-curves are pretty standard. Invest upfront, get customers, make the money back and then some over time. But they only work in this case if Spotify can improve the margins it makes on each of those customers, and that’s where the third J-curve comes in.

Spotify’s third J-curve comes from investing upfront to backwards integrate into supply. Just like Zillow spooked investors by announcing that it would buy and sell houses in an attempt to turn its data and distribution advantages into larger profits over time, Spotify has recently spooked investors by spending $650 million to acquire companies across the podcasting ecosystem. Spotify is attempting to use those investments to drive better economics over the long-term.

Spotify is willing to take losses in the short-term because it is looking to a future in which audio is much larger than it is today. Its ability to generate profits in that future is tied to the success of its podcast strategy.

Podcasts and Earshare

Spotify’s strategy can be boiled down to three steps:

Be consumers’ go-to audio player.

Convert free customers to paid subscribers.

Get customers to spend more of their earshare listening to non-label-owned content, particularly podcasts.

Podcasts are crucial to all three.

Spotify is making great strides on becoming consumers’ go-to audio player. They have 271 million monthly active users, and user acquisition has begun accelerating again over the past three quarters after slowing down over the previous three years. Podcasts have not played a huge role in customer acquisition. The growth in MAUs is better attributed to the 90-day free trials, superior product (I switched all of my listening over to Spotify at the end of 2019 when the Apple Podcast player crashed every time I tried to play an episode), and marketing coups like Wrapped.

Podcasts, though, have been big for getting those monthly active users to get even more active, to stay that way, and convert to paid subscribers. In its most recent letter to shareholders, the company wrote,

We have a growing body of evidence showing that there are significant benefits to engagement, retention, and conversion of users from Ad-Supported to Premium stemming from consumption of Podcast content. We have seen benefits to retention on the order of several hundred basis points, which is a material change on a retention curve, for users that engage with spoken word content relative to those that haven’t, and early data indicates that these users are more likely to convert to Premium over time.

Personally, the story checks out. When I began listening to podcasts on Spotify late last year, I went from using Spotify once in a while to using it multiple times per day. Now, anything I listen to is in one app, and I can’t imagine getting rid of my subscription. I’d even stick around through price increases.

Most importantly, though, my listening to podcasts on Spotify means that I spend more of my earshare in the app on content that they don’t need to pay rightsholders for.

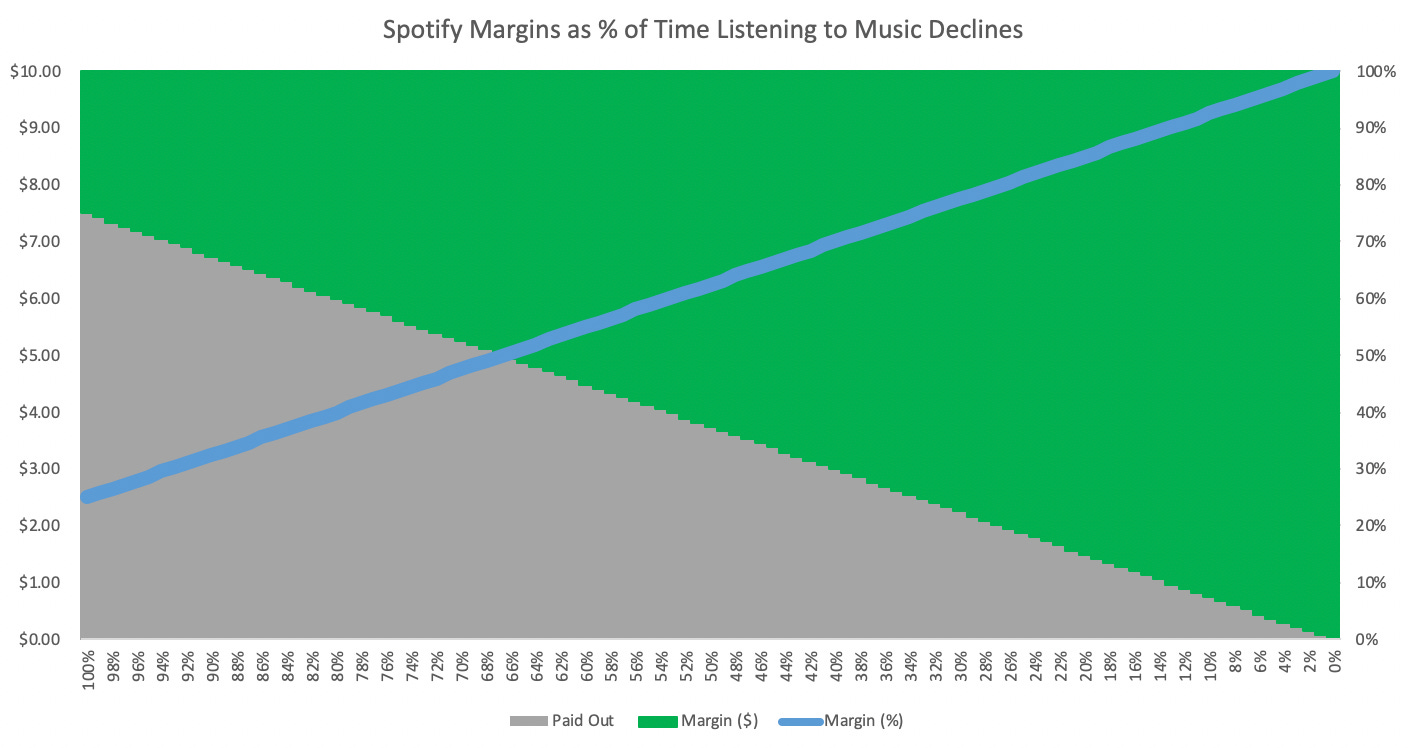

To be honest, it’s unclear to me whether under the current agreement with the labels, Spotify needs to pay out ~70% of all subscription revenues to the labels, or just 70% of the revenue proportional to the amount of time spent listening to music. If it’s the former now, I suspect that Spotify’s biggest push in upcoming negotiations will be to move it to the latter from here on out. They want to be in a position in which more time listening to podcasts means less money paid out to labels.

In a world in which Spotify only has music, the narrative about its being a slow-growth, low-margin business is largely true. It’s locked into the low-margin left side of the graph below. But as Neil Cybart wrote in Spotify is Evolving on Above Avalon, “One of the primary goals in developing an audio platform consisting of podcasts is to generate higher gross margins by having subscribers spend time listening to something other than music.” As podcasts take more of listeners’ earshare, Spotify is able to capture increasingly higher margins and begin to crack the narrative.

Podcasts might represent an even bigger opportunity for Spotify than just capturing higher margins from existing users. Podcasts could open up a path for Spotify to do to audio what Google did to the internet.

In Will Spotify Ruin Podcasting?, Matt Stoller wrote that, “Spotify is directly mimicking Google and Facebook, and attempting to roll up power over digital audio markets the way Google and Facebook did over the internet. It has already done so in music.”

In Spotify Earnings, Podcasts and Lifetime Value, The Ringer Acquisition, Ben Thompson laid out how that might work:

First, while music is very centralized, podcasts are very decentralized, much like the Internet used to be. That meant there was a large opportunity to aggregate podcast listeners much like Google aggregated web users.

Second, the payoff to centralization and aggregation was not simply in charging a monthly subscription, but potentially more lucratively, to building a dominant podcast advertising service for not just Spotify podcasts but independent podcasts as well.

Just a few years ago, if you had told someone that podcasts were the key to a hundred billion dollar business outcome, they would have laughed at you and then asked you what a podcast is.

But podcasts have become a large and rapidly growing market - monthly listeners have doubled over the past five years, and over 51% of Americans have now listened to a podcast. (Check out a16z’s Investing in the Podcasting Ecosystem for more eye-popping stats) Spotify is laying the foundation to monetize the podcast market while Apple gives it away to focus on larger current opportunities, like selling $9 billion worth of AirPods alone. In this context, Spotify’s rationale for acquiring The Ringer and Gimlet media becomes more clear.

Because Spotify has data on all of its users, it can theoretically target podcast listeners with more relevant ads. As it serves more relevant ads, as Daniel Ek said, “you generally can raise CPMs across the board, because advertisers feel more certain about the results that they’re getting.” As it gives advertisers a more targeted way to reach local consumers, it can steal share from local radio.

The global radio advertising industry is a $35 billion industry. Based on the earnings of the top 10 radio stations in the US, spoken word radio stations (news/sports) account for 57% of revenues. Applying that same percentage to the overall market, spoken word audio advertising is a $20 billion market before applying any sophisticated data or targeting.

For context on what data and targeting can do to grow the revenue pie, the US newspaper industry generated $37.8 billion in advertising revenue in 2008, the year that Google acquired DoubleClick. In 2019, Google generated $161 billion in revenue - more than four times what the entire U.S. newspaper industry made combined eleven years earlier. The prize for Spotify becoming the Google of Audio is huge.

But in order to get there, it needs to prove that it can generate more money for podcast creators and better results for advertisers. To do that, it will start by serving dynamic ads on the very popular audio content it owns as a result of its Ringer and Gimlet acquisitions. Once it proves superior monetization capabilities on itself, it can provide those same services to third-party podcast creators.

No company has the distribution, data, assets, and focus on audio that Spotify does. It has spent to acquire users by taking low margins on music and by offering free trials and it has spent to acquire podcasts and companies that provide the tools to podcasters.

We’re in the trough of the J-curve, the spot where the numbers look the worst. Once we begin seeing signs that we’re emerging from the trough into the upwards trajectory, that the “low-margin/slow growth music service” narrative is cracking, the stock will break out of the $120-160 no man’s land it’s been languishing in since IPO.

The insiders, those people who understand the narrative best, seem to agree. Spotify launched a $1 billion buyback in late 2018, and in July 2019, Ek bought $16 million of warrants that would require the stock to break $210 by July 2022 just to break even.

Investing in Narratives

Remember up top when I said that the numbers are all priced in and that the upside is in the narrative? Think about it this way.

What’s easier for a finance professional or a computer to model?

$77 million in operating losses with low margins and declining revenue per user

or

Everything that I wrote up to this point

The answer is A. And in Spotify’s case, when the numbers don’t look so good, that’s going to be reflected in the stock price. My bet is that not everything in B is.

Making matters worse, even Spotify’s CEO admits that, “History has shown us that while we’re usually right in predicting the outcome of our strategy, exact timing can be uncertain."

The beauty of investing on counter-narratives, though, is that it doesn’t take the full story to play out for the stock to rise. All it takes is signs that the prevailing narrative is cracking for other investors to wake up to the possibility that the future might play out differently than they expected.

Slack is my favorite example of this. For Slack, the narrative has been that Microsoft Teams would prevent Slack from winning large enterprise accounts, capping its upside and profit potential. Two of the largest positive moves in Slack’s share price happened on the days that the narrative showed signs of cracking, when the market learned the IBM and Uber had their whole teams collaborating on Slack. The story is far from over, Slack is only two companies closer to proving that it can sell to enterprises, and the company didn’t adjust guidance on the release of either piece of news. All it took was signs that they might actually be able to pull off the crazy thing they said they would be able to pull off for the market to turn bullish.

I think we’re going to see the same thing happen with Spotify. Spotify will stay unprofitable and low-margin for a while yet, but the price will rise on cracks to the bearish narrative.

We will start to hear more from the company about the increasing earshare going to podcasts instead of music. We’ll hear leaks that with more users, they have more leverage over the labels in their upcoming negotiations, and that that leverage might allow them to change the structure of the revenue share. We’ll hear that Spotify will only need to pay the labels in proportion to the amount of time users listen to their music, not as a percentage of total revenue. We’ll hear more about the positive impact that podcasts are having on conversion from free to paid subscriptions. We’ll hear about the ad rates Spotify is able to command on its owned podcasts by dynamically targeting ads, and we’ll hear about early deals that Spotify is cutting with some of the most popular podcast networks to do the same for them. We’ll hear publications with larger reach than Ben Thompson or Matt Stoller asking whether Spotify is the Google of the rapidly growing audio market.

We will hear a bunch of quiet signals that a new narrative is taking hold. And at that point, investors won’t be the only ones listening. If Spotify is able to turn its user data and recent acquisitions into early signs of an audio advertising business, the boardrooms at Disney, Facebook, Google, Amazon, Microsoft, and Netflix will be listening with their checkbooks in hand, too.

Post-Roll

Obviously the Coronavirus could kill this whole thesis. It’s choppy out there. Be careful. Etc… But as someone who works from home, I can tell you, I listen to a lot of podcasts.

Have thoughts on this topic? Vehemently disagree? Come discuss it on Twitter.

Links & Listens

🤑 Investing in the Experience Economy | Mercedes Bent | Lightspeed

Mercedes Bent, a Partner at Lightspeed, uses Pin & Gilmore’s “Four Realms of an Experience” to map the Experience Economy. Bent cites three trends shaping the move from goods to experiences:

Social is the new search.

URL (online) isn’t enough. IRL (In Real Life) is bouncing back.

Retail needs a savior.

Amen.

🏬 On Neo-Traditional Development | Web Smith | 2pm

Web agrees that retail needs a savior, it just isn’t who you’d expect.

Victor Gruen, the father of the American shopping mall, had a vision for spaces that mixed retail and experiential to strengthen local communities. The mall, obviously, has fallen short of that vision, but its recent struggles create new opportunities. One of the brands looking to bring experience and community back to the mall? Blockbuster. Yes, that Blockbuster, might be retail’s savior.

🧮 The Business Equation | Brett Bivens

Bivens looks at Benchmark, Amazon, eBay, Ro, Roku, PayPal, and Peloton to tease out their business equations - the simplified set of factors that the companies’ teams use day to day to guide decision making. It’s amazing how much complexity underlies these simplified equations.

🗑 Garbage Language | Molly Young | Vulture

Why do we talk the way we talk at work? Young has some thoughts.

“No matter where I’ve worked, it has always been obvious that if everyone agreed to use language in the way that it is normally used, which is to communicate, the workday would be two hours shorter.”

What’s Next?

After a fun first week in the Not Boring Slack group, we’re kicking off IRL meetups this week with a series of welcome dinners. We’re also starting a Book Club and a Writing Club, with more on the way. If you want to get involved, apply here.

If you’re enjoying Per My Last E-mail, help me out by forwarding this e-mail to the one friend you think would find it most interesting. Or take the wide net approach by sharing the subscribe link on Twitter or LinkedIn.

Thanks for reading,

Packy