Zoom's Blank Check

Zoom's Blank Check

A Case Study: What to do when you have an expensive stock and no moats

Welcome to the 870 newly Not Boring people who have joined us since last Tuesday! If you’re reading this but haven’t subscribed, join 14,377 smart, curious folks by subscribing here!

🎧 To get this essay straight in your ears: Zoom Blank Check (Audio) or on Spotify

Hi friends 👋,

Happy Monday! I hope all of you had a great weekend and got to spend some time away from Zoom. It’s Monday now, though, and Mondays mean Zoom.

Because we all live and work on Zoom, everyone talks about it. We talk about Zoom fatigue, sure, but some of us nerds also talk about how expensive Zoom’s stock is and whether or not it has any moats that will protect the business after COVID passes and competitors catch up. What we don’t talk about as much is what the company should do about it.

Today, we’re going to change that with the first Not Boring Case Study.

But first, a word from our sponsor.

Today’s Not Boring is brought to you by… Barrel

Last year, when people still gathered in person, I went to a Write of Passage meetup in NYC. I spent most of the night talking to a couple of people, one of whom was (and still is) Peter Kang. Peter told me that he ran a creative and digital marketing agency called Barrel. Said it was doing well, didn’t brag. Then I got home and looked it up. Peter was being humble.

Barrel is a 32-person team of designers, developers, strategists, and producers who have worked with clients like Barry’s, Dr.Jart+, Bare Snacks, ScottsMiracle-Gro, Rowing Blazers and many more to build their Shopify sites and marketing strategies across email, paid, and SEO.

You know how I feel about companies forking their dollars straight over to Google and Facebook with shitty creative and unoptimized campaigns. Please don’t do that. Work with Peter and the Barrel team.

Now let’s get to it.

Zoom’s Blank Check

You Think You Know Zoom

Zoom has grown spectacularly during COVID. It is the best video conferencing software on the market and is perfectly designed for viral growth. Its numbers are mind-blowing, and it deserves to be one of the best performing stocks in the world.

Having said that… $ZM (the stock) is also incredibly expensive. Worse, many, yours truly included, worry that Zoom has no moat.

It me ^^

No moat means that Zoom is open to attack from all angles.

Google can increase the size of the Meet button until it takes up the whole calendar.

Microsoft can do the Microsoft thing and bundle video with Teams.

A wave of startups can come in and pick off verticals.

At best, the argument goes, Zoom will have to lower prices to retain customers. At worst, it will lose them to free, bundled, or more use case-specific competitors. Easy come, easy go.

But I’m coming around on Zoom’s long-term prospects, if it makes the right moves in the coming months, because I think it may have stumbled into a truly brilliant strategy.

Before we get there, though, we’re going to start with a case study. Today, you’re Zoom’s CEO, Eric Yuan.

Your company has put up historic numbers because of your single-minded focus on the customer and your product’s quality and virality.

Competitors are coming at you from all sides, and you’re easy to attack because you haven’t built moats around your business.

Your stock is expensive by any measure.

I’m going to ask you to give me your ideas after the case study before giving you mine. Here’s the question you need to answer:

What do you, as Zoom’s CEO, do to maximize long-term shareholder value?

Zoom Case Study

Zoom’s Unprecedented Ascent

You’re all familiar with Zoom the product at this point in the quarantine, but you might not know as much about Zoom the company. Compared to my recent profiles on Tencent and SoftBank, the Zoom story is dead simple, because the company has focused on customer happiness through product and engineering to the exclusion of almost everything else.

In 1995, a Chinese engineer named Eric Yuan went to Japan to see Bill Gates speak. He was so inspired that he decided then and there to move to Silicon Valley. He applied for his H1-B visa and was denied eight times before the US granted him a visa on his ninth attempt.

When he arrived in the States, he went to work for an early video conferencing software company, WebEx, where he served as a founding engineer then VP of Engineering for nine years. The company IPO’d in 2000 and Cisco acquired it six years later for $3.2 billion in cash.

He stayed on at Cisco in the same role for four years, but became increasingly unhappy. As he explained to Bessemer partner Byron Deeter:

Every time I talked to a WebEx customer, I felt very embarrassed, because I did not speak with a single happy WebEx customer.

He realized small tweaks wouldn’t fix WebEx, so he pitched the Cisco execs on rebuilding it from the ground up. When he failed to convince his new bosses, he left to start his own thing.

After leaving WebEx, according to the Acquired podcast, “a whole cadre or basically anyone who had ever worked with Eric immediately gives him money, just blank check, to back him to work on whatever he’s going to do.” He started building SASB, a consumer application built on top of video chat, but he quickly realized that building an application on top of a crappy product wouldn’t make customers happy. He knew what he needed to do: rebuild video chat from the ground up.

History doesn’t repeat itself, but it rhymes. Just like critics scream that competitors will topple Zoom today, everyone told Yuan that his idea wouldn’t work because video conferencing was too crowded even then.

But he did what he does -- talked to customers -- and realized that if none of them were happy with their current solutions, there was room for a product they’d actually like. He founded Zoom in April 2011.

Turns out happiness mattered, particularly at that moment in time. On the Acquired podcast, Zoom investor Santi Subotovsky, pointed out that enterprise SaaS purchasing decisions moved from the IT department to the end user around that time. When the purchasing decision is made by the people who have to use the product, the battlefield moves from sales to product quality. And Zoom had the best product, even in its earliest days.

In August 2012, the week Zoom launched, famed tech journalist Walt Mossberg wrote, “my verdict is that Zoom.us is a very good product with lots of practical uses.”

Source: All Thing D

A less well-known trendspotter, My Mom, started singing Zoom’s praises in 2013. She facilitates large group meetings with participants from across the globe, and couldn’t stop raving about Zoom. She gave the same review that so many have since: “It just works.”

Unfortunately, she wasn’t able to get an allocation in Zoom’s $6 million January 2013 Series A, its $6.5 million September 2013 Series B, its $30 million February 2015 Series C, or its $100 million January 2017 Series D. Sequoia led that one, at a $1 billion valuation, back when $1 billion meant something. At the time, Techcrunch wrote:

Zoom, which has over 400 employees, will likely expand with the massive new investment, but Yuan wasn’t going to commit to anything just yet. He describes himself as “a conservative entrepreneur” and he will bank the money and invest in the parts of the company that require it, as the time is right.

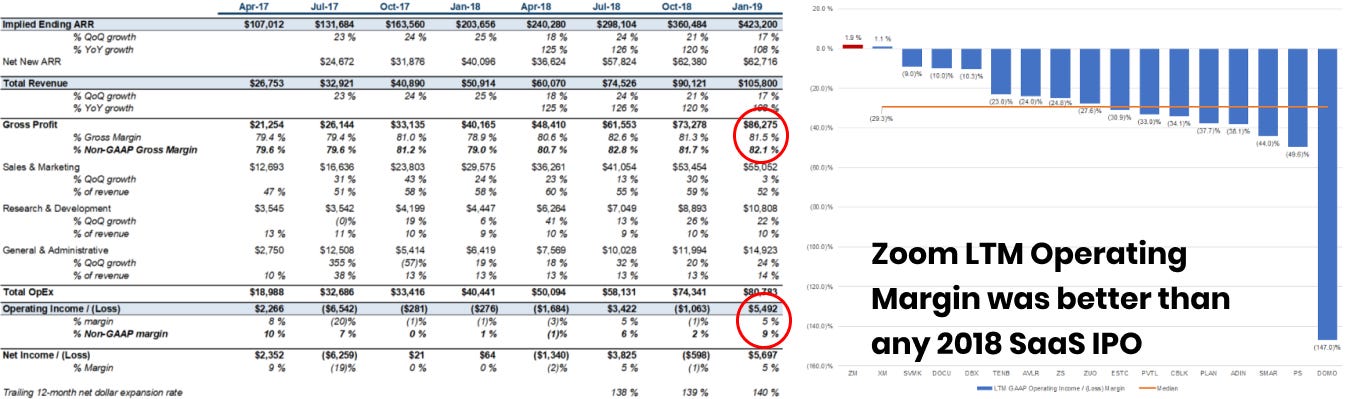

When Zoom filed its S-1 in April 2019 to announce its intentions to go public, Yuan’s conservative stewardship of the company jumped off the page. Zoom’s profitability was a welcome anomaly in a year dominated by IPOs from cash-burning companies like Uber, Lyft, Slack, and Beyond Meat. Alex Clayton highlighted Zoom’s 82% gross margin and 5% operating margin in his excellent Zoom S-1 Breakdown:

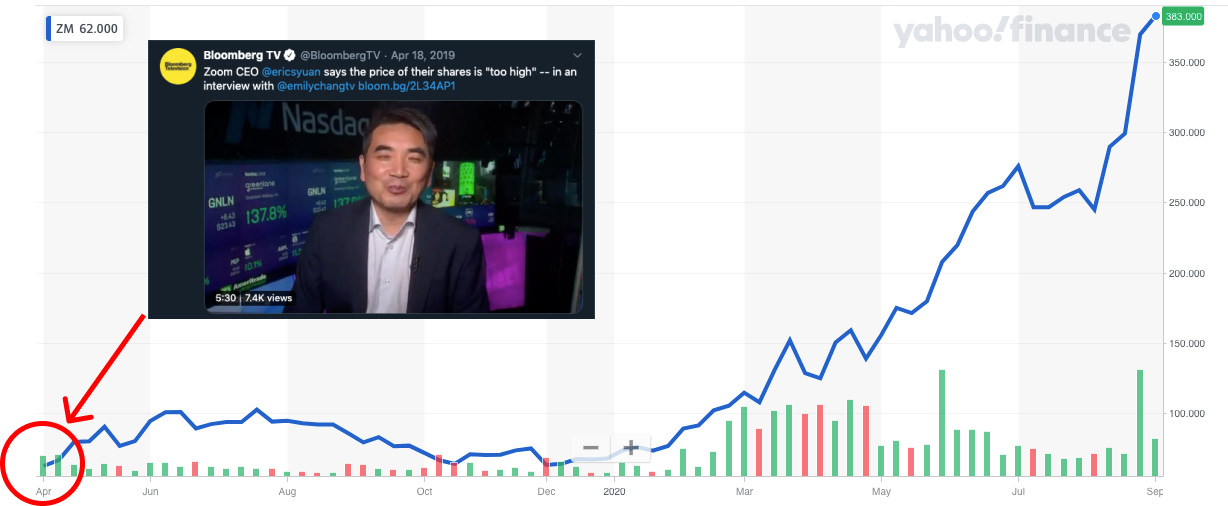

Investors proved how much they loved a profitable IPO when Zoom went public on April 18, 2019. Priced at $36, its shares popped as high as $66 on IPO day before closing at $62. Its market cap jumped from $9.2 billion to $15.8 billion in one day.

That day, Yuan told Bloomberg News, “The price is too high.”

It’s gotten a little higher since then, because it was prepared for the unprecedented.

Zoom is Overvalued

On May 11th, I wrote a piece called While Zoom Zooms, Slack Digs Moats. I was perplexed by the fact that Zoom was up 106% since the first COVID case was reported on January 21st while Slack was only up 33%.

Welp, here we are four months later, and Zoom is now up 399% since the start of COVID while Slack has dipped, and is only up 15%. Listen to me at your own peril!

Since I wrote that piece in May, Zoom has somehow accelerated. It reported absolutely absurd numbers on August 31st:

Q2 revenue of $664 million, up 355% YoY.

458% YoY growth in companies with more than 10 employees

130% Net Dollar Expansion Rate (how much it grows revenue from existing clients)

2,079% YoY Free Cash Flow growth, from $17.1 million to $373.4 million

That huge spike you see in the chart above on the right side of CEO Eric Yuan’s face is the market reacting to those earnings. The price shot up so much the day after earnings that it briefly passed even the most out of the money call option strike prices.

Zoom deserves its success. It’s a spectacular company, with a potent combination of growth and profitability. In Software-as-a-Service (SaaS), there’s something called the “Rule of 40” that says a company is doing well if its growth rate + profit margin add up to over 40%.

This past quarter, Zoom’s added up to 411%. Zoom 10x’ed the Rule of 40 🤯

But it’s possible to be both incredibly excellent and incredibly overvalued.

You can’t judge whether a stock is expensive by its share price or enterprise value alone, you need to look at how its price or enterprise value compares to its revenue and earnings (multiples) and how those multiples compare to similar companies (comps). Zoom is expensive by nearly any measure.

On the earnings side, it’s trading at a Price to Earnings (P/E) multiple of 489x, second only to Tesla (and Shopify, which is not yet profitable) among the largest 75 companies by market cap.

Looking at revenue, its Next Twelve Months Enterprise Value / Revenue (NTM EV/Rev) multiple is 37.6x. According to TIKR, the average for comparable software companies is 8.4x. For comparison: Slack trades at 14.1x, Microsoft trades at 9.5x, and Apple trades at 6.2x. The two highest I found aside from Zoom are Zscaler at 27.7x and Okta at 26.6x.

But there’s a good reason that Zoom’s stock trades at higher multiples than comparable companies: it’s growing much faster.

Even if it looks expensive based on its revenue projections for the next year, it might not look so expensive based on revenue in three or five years if it keeps doubling. That’s what the Zoom bulls say. Sure, Zoom is expensive now, but it’s going to keep growing its market share in video communications while the total video communications addressable market continues to grow.

Bears have one consistent answer: Zoom has no moats.

Zoom has No Moats

When I wrote that (for now!) ill-fated piece in May, my argument was that, “Zoom traded moats for speed.” The same reason that so many people were able to start using Zoom so easily -- you can join a Zoom with just a link -- is the same reason that Zoom is in trouble.

There are two questions to ask regarding Zoom and moats:

Does Zoom have moats?

Does it really matter?

We’ll handle the second first.

Moats are important for any company that wants to sustain profitability over time. They’re massively important for companies that are mostly valued based on future earnings, like Zoom. The higher your multiple, the more the future matters. It’s valued at $109 billion today because the market believes it can sustain and grow earnings for many, many years to come. To do that, it needs moats.

“Moat” does not mean “advantage” or “something a company does better than its competitors.” Here at Not Boring, we subscribe to the Hamilton Helmer School of Moats. In 7 Powers, Helmer defines moats as “barriers that protect your business’ margins from the erosive forces of competition.”

Advantages are static, moats are dynamic. A company can have an advantage today and lose it to the forces of competition over time.

Everyone agrees that Zoom has an advantage today, but does it have moats?

After Zoom’s tremendous Q2 earnings and the subsequent pop, Morning Brew COO Austin Rief asked what Zoom’s moats are, and got a lot of responses:

Brand was the most commonly-cited moat, followed by product, or the idea that “it just works.” I’ll take each in turn.

Brand. “Zoom is a verb! Like Google!” this argument goes. That’s true, and it’s not necessarily a brand moat. When’s the last time you Instant Messaged a friend on AIM?

The Helmer definition of Brand is “The durable attribution of higher value to an objectively identical offering that arises from historical information about the seller.” Think Tiffany’s. It can sell the exact same product as Zale’s for 4x the price because that Tiffany Blue box means something to people. If Google Meet catches up and offers an “objectively identical offering,” and puts a big blue link to it right in the calendar, and offers it for less than Zoom, most people are going to go with Google Meet.

Product. Superior product isn’t a moat. Once more, for those in the back, superior product isn’t a moat! A superior product is an advantage. Moats are needed to protect that advantage. Google, for example, turned a superior product into network effects - the more people who use Google, the more searches it handles, the more likely it is to give you the best results.

In What Comes After Zoom?, Benedict Evans compares Zoom to two other companies that won in crowded spaces by building superior products: Dropbox and Skype. But a superior product didn’t protect either company. Evans wrote that two things happened to Skype, which did the same thing for VOIP that Zoom has done for video:

Its product drifted for a long time and user experience declined.

Everything has voice now, so voice is a commodity.

He argues that the same thing will happen to video, and that the companies that win the next phase of video won’t be the ones who ask, “How can I make the tech better?” The tech will be a commodity. The winners of the next phase will be the ones who use video to build experiences that solve particular user needs.

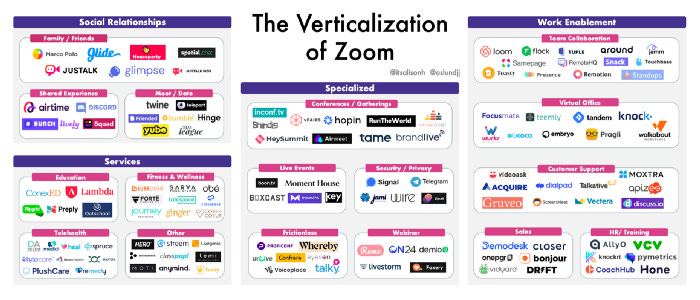

Without a moat, Zoom is open to attack from those companies. In The Verticalization of Zoom, JJ Oslund highlights all of the companies that are taking advantage.

Each thing that we did on Zoom in the beginning of quarantine -- game nights, school, casual hangouts, dating -- is getting its own app.

Although Zoom has an API and SDK, most of these new companies don’t build on Zoom.

Akarsh Sanghi, who recently launched a video streaming platform for lifestyle creators called Reach.Live out of YC, told me that all the new YC companies are building on the same stack:

“React application on the client side, typescript, hasura, Postgres, WebRTC and Agora APIs for the video player.” Everything is adding video, and Zoom isn’t involved. Its competitive advantage is showing the earliest cracks.

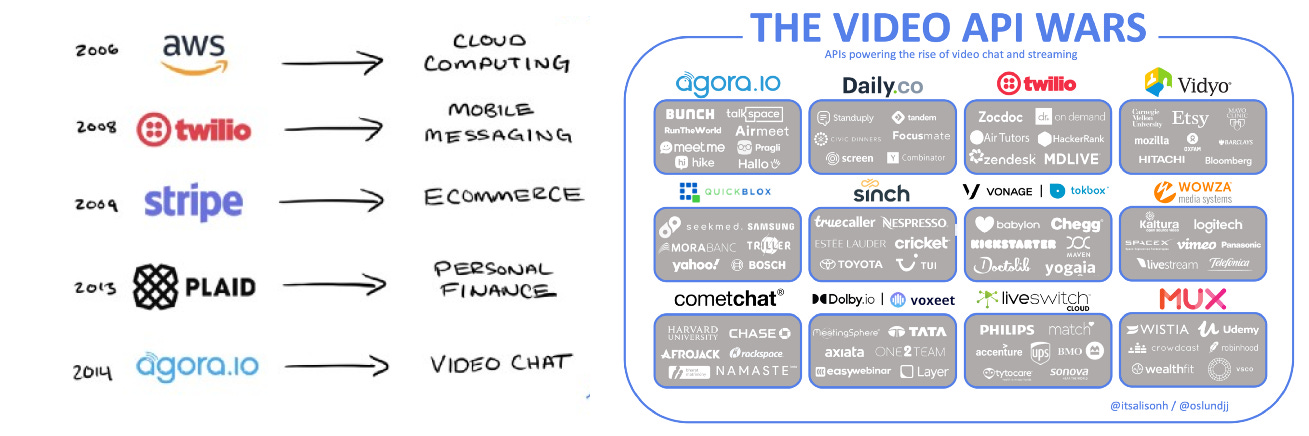

Oslund wrote about this too, in The Unbundling of Zoom, in which he describes the landscape of APIs that are making it easier than ever to build video chat applications.

Because of the rise of video APIs like Agora, companies that are trying to build verticalized product to steal little bits of demand from Zoom don’t need to start from scratch every time. They plug in reliable video in a few lines of code, and spend their time and resources on building out a user experience that resonates with their specific group of target customers.

Until now, the fact that Zoom “just works” has been its defense against bigger competitors. Now, though, Agora is arming the rebels and giving everyone video that “just works.” The rebels are mounting the first serious attack on Zoom’s castle.

But Zoom has a massive lead and a fully-stocked war chest. What it does in the coming months and years will determine whether it goes the way of Skype or makes its $109 billion valuation look cheap.

So What Would You Do?

Here’s where Zoom is today:

Rule of 400! Zoom’s growth and profitability are historically strong.

Dubious Moat. At best, Zoom has weak moats and is open to attack from competitors big and small, which could slow growth and erode margins.

Expensive Stock. Zoom is more expensive than nearly every comparable company on a PE or NTM EV/Rev basis.

This isn’t someone else’s champagne problem, it’s yours. Remember, you’re Eric Yuan for the day. What do you do to maximize long-term shareholder value?

We’re trying something new today! I want to hear what you would do if you were Eric Yuan. Fill out this short form with your thoughts:

Party Like It’s 1994

Blank Check was the first movie that made me want to be rich. I was seven when the movie came out in 1994, just old enough to appreciate the power of a million dollars.

If you haven’t watched Blank Check in 26 years, this will jog your memory.

Blank Check Trailer, Recut with the Requiem for a Dream Theme

For our purposes, what’s important is that a kid got a blank check and spent $1 million really quickly on way more than $1 million worth of stuff. Now $1 million in 1994 is like $1.748 million today, but what Preston was able to buy with $1 million is truly astonishing:

A castle in Austin, TX which has a current Zestimate of $4,657,416

A go-kart racetrack

Jewelry for his adult girlfriend

Night on the town in a limo

Massive wall of TVs

State-of-the-art home office

Mr. Macintosh speech system

Unlimited snacks

A $100k party

And more!

All in all, that’s about $5 million worth of stuff for $1 million.

When the villain, Carl Quigley, gets a hold of Preston, he stares him down and asks, in shock, “How could you spend a million dollars in six days?”

Easy answer, Carl. Preston realized that the market was somehow overvaluing his dollars and spent it before anyone realized that they were giving him like an 80% discount on everything.

I tell you all of this not only out of a sense of nostalgia, but because Zoom is Preston Waters right now.

Zoom is an excellent company with extremely strong product and engineering chops and a stock price that essentially gives it a blank check. By focusing on short-term profitable growth, Zoom has stumbled into a brilliant position:

Abandon moats in exchange for growth via superior product and distribution

Grow share price to an inflated level

Use valuable stock to buy moats

Zoom is one of the fastest companies ever to reach a $100 billion market cap, behind just Google and Facebook. Both of those companies have aggressively used their valuable stock to neutralize threats and fuel growth through acquisition. Zoom needs to do the same.

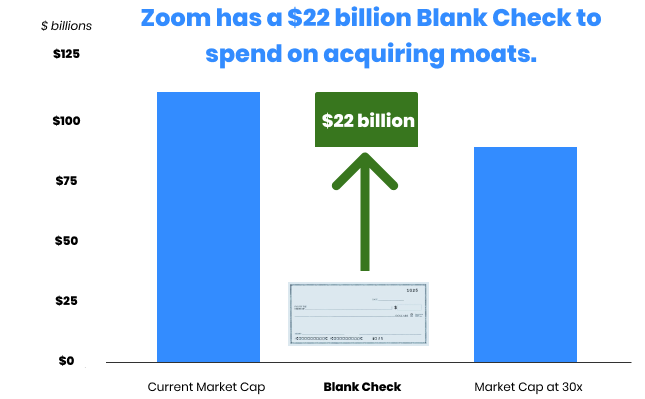

How Blank is Zoom’s Blank Check?

Eric Yuan is rational. Remember that he said Zoom was overvalued on the day it IPO’d. I’d imagine he thinks it’s overvalued today, too. The difference between what he thinks his company should be worth and what the market values it at today is his “Blank Check.”

Let’s say that, because of its breakneck growth, Zoom does deserve a higher NTM EV/Rev multiple than any of its competitors. Remember that Zscaler was the next highest at 27.7x. Let’s give Zoom something like 30x. The difference between its 37.6x multiple and 30x is 7.6x, which represents about $22 billion in EV.

Zoom should go on a $22 billion Preston Waters-esque spending spree. Instead of houses, limo rides, snacks, and TVs, Zoom should acquire moats.

Because potential targets realize that Zoom’s stock is expensive, as well, they’re unlikely to treat $1 worth of Zoom stock and $1 worth of cold hard cash the same. The market would be friendlier to a secondary offering. So Zoom should sell new shares and raise at least half of that $22 billion Blank Check in cash.

For simplicity’s sake, let’s all agree that Zoom has $22 billion of cash and stock to spend on acquisitions, k? Good. Now what should it buy? It’s Fantasy M&A time, y’all!

WebEx Reunion

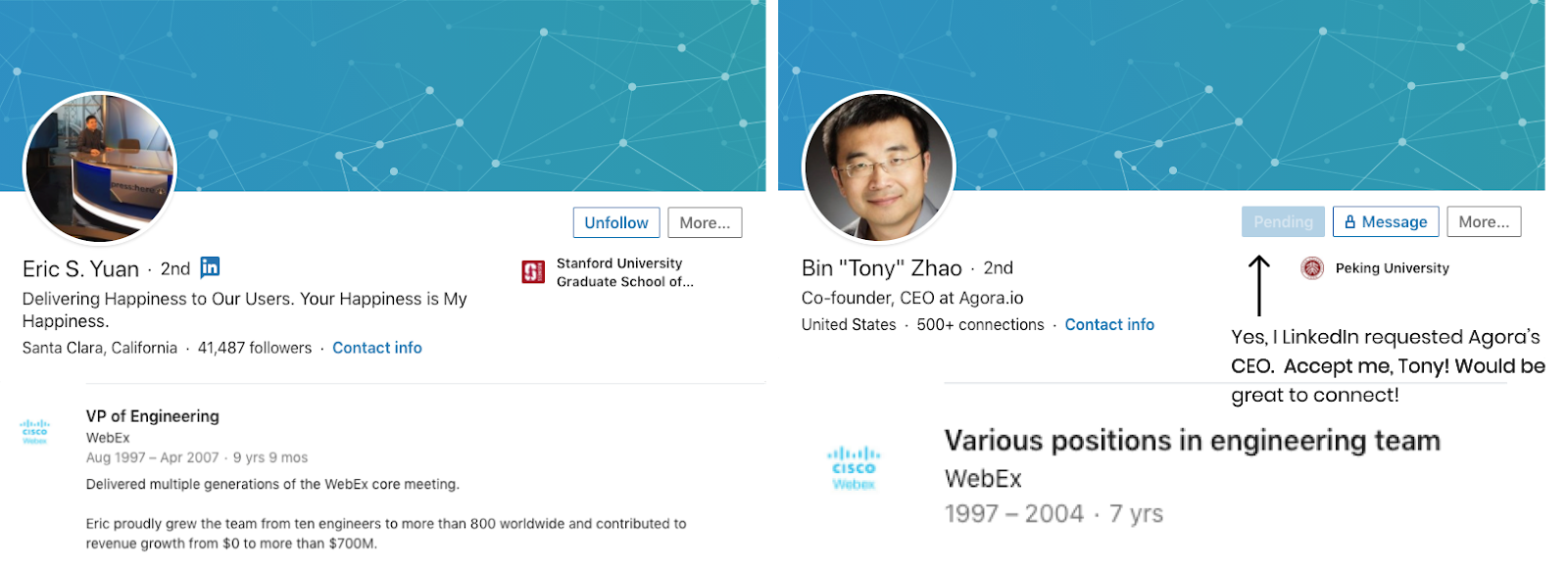

Zoom needs to buy Agora. It’s a bigger threat than Google or Microsoft, it would give Zoom moats (switching costs and scale economies), and it would be a reunion.

There was something in the servers at WebEx in 1997. That year, two talented engineers joined the video conferencing pioneer as founding engineers: Eric Yuan, who you’re now acquainted with, and Bin “Tony” Zhao, the co-founder and CEO of Agora.

Zhao left right around WebEx’s IPO in 2004, for the same reason Yuan would leave seven years later. He said that after releasing the audio streaming product he worked on at WebEx, he "started receiving so many complaints: their session was cut off, the quality was bad, and so on.”

While at Chinese social media company YY, Zhao realized that:

If someone could provide an easy integrated API to support that capability, application builders everywhere would have less barriers in using real-time audio and video in their apps. This would open up a world of possibilities and use cases.

He was that someone. In 2013, Zhao left YY to start Agora, which bills itself as the “Real-Time Engagement Platform (RTE-PaaS) for meaningful human connections.”

Agora offers a Software Development Kit (SDK) and Software-Defined Realtime Network (SD-RTN) that developers access through its Application Programming Interface (API) to build video communication into their products. Got it?

In English: Agora lets developers easily add real-time or broadcast video into their products with a few lines of code. You can think of it like Stripe for video. Developers can add video to their product as easily as they add payments, allowing them to focus on their own unique differentiators.

As a result, a new wave of startups is solving specific customer needs with video by plugging in Agora.

Agora’s customers include well-funded companies like Michael Phelps-endorsed therapy platform, Talkspace, and a16z-backed events platform Run The World. Neither Talkspace nor Run the World is a threat to Zoom on its own. The threat to Zoom is that thousands of companies plug Agora into their products and offer a better experience for the thousands of use cases that people use Zoom for today.

This is where Zoom’s lack of moats hurts. Customers can leave easily when a new product better suits their needs. That’s true for more niche uses like therapy and events, but also for Zoom’s core focus areas like work and education.

When new entrants don’t need to build the tech from scratch, they can spend all of their time and resources building better experiences for every use case, work and education included.

The move is offensive as well as defensive. By buying Agora, Zoom can set its sights beyond the office into a wider variety of use cases, without having to build a single use case-specific feature. Agora might also be Zoom’s ticket to the Metaverse.

As I wrote about in Tencent’s Dreams, I don’t think that any one company will own the Metaverse. Instead, it will consist of interoperable products built on top of a number of key platforms: Epic for virtual worlds, Snap for AR, Spotify for Audio, and maybe, Zoom/Agora for video.

An Agora acquisition would:

Neutralize the threat represented by the Verticalization of Zoom

Allow Zoom to participate in the upside of the Verticalization of Zoom

Give Zoom a better foothold into the new use cases and the Metaverse by becoming the platform on top of which thousands of companies build video-based products

Importantly, acquiring Agora would allow Zoom to build moats. Agora gives Zoom an API product, like Stripe. API products have at least two strong moats:

Switching Costs: Once you build your product on top of Agora, you’re unlikely to rip it out and switch to a new RTE-PaaS solution.

Economies of Scale. Just as Stripe can develop features and capabilities to serve edge cases and spread development costs over millions of customers, Zoom/Agora would be able to spread the cost of developing increasingly cutting edge video features over thousands and eventually millions of customers.

The best part? Zoom could acquire Agora for about a third of its Blank Check. Agora, which went public in June, traded up 145% on its first day as a public company, and has stayed relatively flat since. It currently has a $4.9 billion market cap. At a rich 50% premium, Zoom could acquire Agora for $7.4 billion dollars and keep $16.6 billion free to buy more moats.

Moat Shopping

With its biggest threat neutralized and $16.6 billion left on that check, Zoom can get creative. Here are three routes it can take:

Triple Down on Video

Zoom can do to video companies what Tencent does with ecommerce ones: give them capital and traffic.

It can invest in or acquire top video-based applications and give them distribution to Zoom’s hundreds of millions of meeting customers. Plus, backed by Zoom and Agora’s engineering teams and data centers, the companies would be able to accelerate the technical capabilities of their products.

A few targets include:

Loomwould fill a hole in Zoom’s offering by giving customers access to seamless, asynchronous video messaging. Loom recently raised $28.75 million in a Series B led by Sequoia, a Zoom investor, and Coutue, an Agora investor, which valued the startup at $350 million. Zoom would likely need to spend about $1 billion to buy Loom. The video messaging history creates switching costs.

Wherebyis a lighter-weight Zoom for SMBs. Yuan cited problems moving non-enterprise accounts onto Zoom quickly during Coronavirus, because enterprises and small businesses have different onboarding processes. Whereby, beefed up by Zoom’s tech, could become Zoom’s solution for more casual use cases, allowing it to optimize the flows for each type of user. Whereby is cheap. It was recently raising at a $15 million cap, and Zoom could probably snatch it up for under $50 million.

Icebreaker. Eric Yuan is all about delivering happiness to customers, and Icebreaker is the most delightful video chat experience I’ve had during quarantine. Icebreaker is perfect for social gatherings for which Zoom is an awkward solution. Icebreaker has raised $7.2 million, and Zoom could acquire it for around $50 million.

Hopinor Run the World. One of the areas in which Zoom falls shortest is in large events. Teachable built its own custom solution for it’s Share What You Know Summit (which you should attend with me). Hopin and Run the World are two purpose built solutions that would give Zoom a product to cross-sell to existing enterprise clients and use to lure new ones. Run the World has raised $15 million from a16z and Founders Fund, and Hopin recently raised $40 million from IVP and Salesforce. It would have to spend $75-150 million to acquire one of these two.

Total Price Tag: ~$1.25 billion

Moats Acquired: Switching Costs, Economies of Scale

Owning Video: Priceless

Remote Productivity Suite

Google and Microsoft are waging constant war on Zoom’s territory with Meet and Teams Video. But Zoom’s rich now, too. It should go on the offensive and acquire productivity tools to build out its own remote productivity suite. I’m waiting for somebody to bundle these tools together, and Zoom would be an interesting dark horse.

Loom. Loom fits here too. Zoom should just buy Loom. Loom by Zoom is fun to say. $1 billion.

Airtable. Airtable is a cloud-based spreadsheet and database tool that was rumored to be raising at a $3 billion valuation in April. Bundling Airtable with Zoom would increase switching costs. Zoom could acquire the company for $3-5 billion.

Notion. Notion is a workplace productivity and collaboration tool that was the buzziest on the market before Roam came onto the scene. Like Airtable, bundling Notion with Zoom would increase switching costs. Zoom could acquire it for $2.5 - $4 billion.

Figma. Figma is the collaborative design tool that I use to make all these sweet graphics, by myself. It’s a delightful product, and Kevin Kwok wrote about why Figma wins here. Figma is the leader in products that skip the hub, like Zoom or Slack, and allow people to work together right in the product. It raised $50 million from a16z at a $2 billion valuation in April, and would cost at least $3-4 billion to acquire. It would give Zoom strong network effects.

Calendly. Zoom’s biggest weakness against Google is that Google can put a big Meet button right in its calendar. While it will be difficult for Zoom to get people to switch calendars, it could control Calendly, the scheduling tool. It’s the next best thing, and it hasn’t raised much outside capital so could likely be had for under $100 million.

Miro. Miro is a collaborative whiteboarding tool that is another early favorite of My Mom, and that has a Zoom integration coming soon. It’s not a strong moat, but the ability to whiteboard and save notes within Zooms increases switching costs slightly and could be a strong Pro feature. Miro raised $50 million in April, and would likely cost around $250-300 million.

A Zoom collaborative productivity suite would have high switching costs and network effects, and cement Zoom’s position as the leading remote communication and collaboration tool for businesses.

Total Price Tag: ~$10 billion

Moats Acquired: Network Effects, Switching Costs

Wild Cards

There are three other companies that Zoom at least needs to look at, although they’re a little more out there and don’t fit neatly into either of the buckets above:

TikTok. Zoom is seemingly the only company not involved in the bidding war for TikTok’s US assets. It couldn’t do it alone, but Zoom could potentially be the tech half of a bid with a financial sponsor. TikTok is the only product that’s been more viral than Zoom, it’s video-based, it attracts young users, and it has high switching costs and network effects. And I know, I know, Oracle “won the bid” to be TikTok’s US tech partner, but I’ll believe that when I see the TikTok on-prem db. Until then, this is still anybody’s ballgame.

Roam Research. Roam just raised $10 million at $200 million, but I have smart friends who think it’s still very cheap, and one who thinks it will be worth more than Google. I’m including this note-taking tool in Wild Card instead of Remote Productivity Suite because it has a steep learning curve and would be more interesting as a purely financial buy until it becomes easier to use or Zoom builds or buys technology to automatically transcribe meeting notes to Roam.

Slack. It pains me to say this, but after another ho hum earnings, Slack’s market cap is at $14.6 billion. Zoom would need to pay a significant premium -- I wrote that I don’t think Slack sells for less than $40-50 -- so it would have to overspend its blank check, but if nothing else, Slack has moats. Slack’s network effects and switching costs would help lock Zoom’s customers in, and Zoom could help Slack with its growth problem. I’d love to see this team take on Google and Microsoft (if Google doesn’t buy Slack first).

So Would They Do It?

We all did this case study together, so we know that Zoom should acquire Agora and a handful of other companies. But will they?

Generally, M&A is not in Zoom’s DNA. It completed the first acquisition in its history in May when it acquired encryption company Keybase to bolster its security. In fact, partially because Zoom is nouveau riche, it’s completed the fewest acquisitions of any technology company worth over $100 billion, and the second fewest per years of existence to Taiwan Semiconductor.

But there are signs that Yuan realizes that he needs to get spendy. In June, Zoom hired its first Head of Corporate Development, Colin Born, who previously ran Corp Dev at Qualcomm, GoPro, and Cypress Semiconductor. In July, he doubled the size of Zoom’s corp dev team by hiring an analyst.

Yuan’s not wasteful; I don’t think he would build out a Corp Dev team to sit on their hands. I think Zoom is going to start acquiring companies. A big question is whether they’ll expand Zoom’s product offerings and build moats, like the ones I highlighted, or if they’ll target businesses that strengthen the core product, like Keybase.

Assuming that Eric and Colin read this, and decide to go the route we suggested here, I’ll address three Agora-specific concerns.

First, Agora is dual-headquartered in both Shanghai, China and Santa Clara, California. In April, Zoom faced scrutiny for potentially routing data through servers in China, and they may be loathe to risk corporate contracts over concerns.

Second, Agora is one of the only companies on the market as expensive as Zoom, at a 33.0x NTM EV/Rev multiple and an eye-popping 4,840x PE multiple (Agora just became profitable in Q1).

Third, and most importantly, Yuan has always been focused on business clients and on providing an excellent experience. Would he be willing to risk defocusing the company and handing over so much control of the user experience to third-party developers?

Those are valid concerns. Zoom’s success has come from relentless focus on the customer, the tech, and the product to the exclusion of competitive threats. It’s worked so far.

But an advantage today is not the same thing as a moat. Zoom needs to protect its business far enough into the future to grow into its massive valuation. For the sake of shareholder happiness, Yuan should put a big number on his Blank Check and hand it to his former co-worker, and some new ones, too.

Thanks to Dan for once again editing and saving all of you from reading my terrible first draft.

Thanks for reading,

Packy

Great article & analysis.

Like the case exercise, and made me even more impressed with how you can clearly lay out the facts and recommendations for complex companies with support